Updated: 25 May 2026

Originally Published: 03 February 2025

For years, PCP and HP agreements were presented as a simple and affordable way to finance a vehicle. Lower monthly payments, fixed contract terms, and flexible end of agreement options made these products attractive to millions of UK drivers.

Consumers who entered into motor finance agreements years ago are finding themselves having to revisit those arrangements in recent months due to new information about the true cost of their deal.

The car finance scandal that has taken the UK by storm has seen significant growth in 2024 as investigations from FCA regulators, court rulings and high levels of public awareness has shone a light on a raft of concerns across the motor finance industry related to non-disclosed commissions, excessive interest rates, subpar affordability checks and unfair sales tactics.

As a result, more motorists are now exploring whether they could be entitled to car finance compensation linked to mis-sold car finance agreements.

The Financial Conduct Authority formally launched its FCA redress scheme on 30 March 2026 [1], creating a structured framework for millions of potential car finance claims involving discretionary commission arrangements (DCAs), high commission models, and other forms of car finance mis-selling.

If you signed a PCP or HP agreement between 2007 and 2024, it may now be worth reviewing your agreement carefully.

This guide explains:

- How to choose the best PCP claims company

- What separates the best car finance claims company from general claims firms

- How claims management companies work

- How to avoid scams

- What finance claims experts actually do

- How a car finance refund check works

- The difference between DIY complaints, solicitors, and CMCs

- What motorists should know before starting a car finance claim

Why Drivers Are Making PCP Claims

Car finance became the dominant way to buy vehicles throughout the 2010s, especially through PCP agreements.

Monthly repayments often looked affordable, but many customers focused mainly on the payment amount rather than the overall borrowing cost or how dealerships were being paid behind the scenes.

As complaints increased, regulators began examining whether dealerships and brokers had unfairly influenced the finance products consumers were offered.

Many complaints now involve:

- Hidden commissions

- Inflated interest rates

- Weak affordability checks

- Poor disclosure of finance costs

- Unclear balloon payments

- Misleading sales explanations

In some cases, dealerships could increase a customer’s interest rate to earn a larger commission from lenders.

Many motorists say they were never told this was happening.

These practices now sit at the centre of the wider car finance scandal affecting millions of UK consumers.

What Is a PCP Claims Company?

A PCP finance claims company investigates whether your agreement may have involved unfair commission structures or other signs of mis-sold car finance.

If issues are identified, the company helps prepare and submit complaints to lenders on your behalf.

Most regulated claims management companies will:

- Review agreements

- Assess commission structures

- Check for unusually high interest rates

- Find evidence to support you

- Deal with lender on your behalf

- Help with complaint processes

- Track FCA redress progress

Consumers often seek professional assistance as older agreements can be hard to trace and even more so where documentation has been lost or when agreements were originated many years ago.

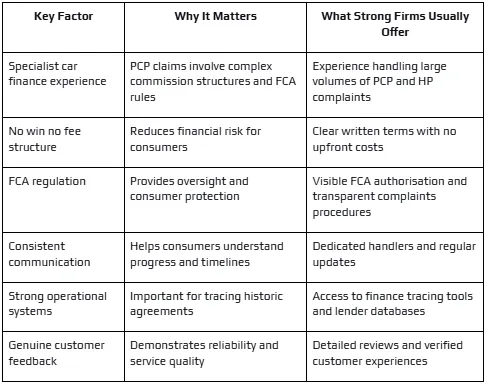

What Makes the Best PCP Claims Company?

Not every firm handles car finance claims in the same way.

Some claims management companies specialise heavily in mis-sold PCP car finance claims and HP complaints, while others handle a wide range of unrelated claim types with limited motor finance expertise.

The best PCP claims company will usually have a combination of:

- Expertise in mis-selling of car finance

- Transparent no win no fee terms

- FCA regulation

- Clear communication

- Dedicated case handling

- Experience in dealing with high volumes of complaints

The best car finance claims company will also explain the process to you clearly without the use of pressure tactics or unrealistic claims.

Consumers should know:

- What fees they will be charged

- Whether VAT is included

- How the FCA car finance redress scheme works

- What evidence may be required

- How long the complaints process might take

- What happens if compensation is awarded

The claims process should not feel like a dark art, it should be transparent and feel easy to navigate.

How to Select the Right PCP Claims Company

Selecting the best PCP claims company isn’t as simple as looking for the largest advert or the first website you find online.

A reputable provider will ensure the process is clear, fair and properly regulated from the outset.

Before signing with any claims management company, ask:

- Are you FCA authorised and regulated?

- Do you charge a fee if my claim is successful?

- Do you charge any upfront fees?

- Will you provide written terms before I agree to proceed?

- Will my case be managed by a dedicated claims team or an associated law firm?

- How will I be kept informed?

- Do you specialise in car finance claims only?

A good car finance claims company should be able to answer these questions clearly and honestly without pressuring the consumer into a hasty decision.

What Defines the Best Car Finance Claims Companies?

The strongest claims management companies usually combine specialist knowledge, clear communication, and proper regulation.

FCA Regulation and the Role of the SRA

The FCA regulates:

- Marketing standards

- Fee transparency

- Consumer communication

- Handling of complaints

- Rules of conduct

Some firms work in conjunction with solicitors or specialist law firms.

Law firms in England and Wales are regulated separately by the Solicitors Regulation Authority (SRA) [3].

Consumers may therefore encounter:

- FCA regulated claims management companies

- SRA regulated solicitors

- Hybrid models involving both claims companies and partner law firms

Any reputable business should clearly explain:

- Who regulates them

- Whether solicitors are involved

- How fees work

- What protections consumers receive

Warning Signs to Avoid

As PCP compensation claims have increased, so has misleading advertising and scam activity.

A good rule of thumb for consumers is to be wary if a company:

- Offers to guarantee you compensation before seeing your agreement

- Persuades you to act on unsolicited calls or text messages

- Uses the small print to hide fees

- Is unwilling or unable to explain how they are FCA regulated

- Pressure you to sign there and then

- Are evasive about who will do the legal work

A reputable PCP claims company should explain the process transparently and allow consumers time to make informed decisions.

How Car Finance Refund Checks Work

One reason many motorists now use claims management companies is because the process has become much simpler than people expect.

A modern car finance refund check can usually be completed in minutes.

Most consumers only need to provide:

- Full name

- Date of birth

- Previous addresses

- Contact details

Many finance claims experts can then trace agreements automatically using credit reference agency data and vehicle registration databases.

This is especially useful for motorists who:

- Moved house

- Changed surname

- Lost paperwork

- Cannot remember the lender

- Took out multiple agreements over several years

At Reclaim247, consumers only provide basic details before systems begin tracing agreements automatically.

The platform interfaces with the large credit reference agencies and vehicle registration databases to find historic car finance linked to the customer. This includes car finance that the customer may have difficulty tracking down.

Once agreements are identified, claims are reviewed individually by partner law firms who gather evidence, negotiate with lenders, and work to maximise compensation on behalf of the customer.

For many motorists, this removes much of the stress involved in managing a car finance claim alone.

Common Types of Car Finance Mis-Selling

The FCA redress scheme focuses heavily on Discretionary commission arrangements (DCAs), where brokers or dealerships could increase interest rates to earn larger commissions from lenders.

The FCA is also looking at:

- Excessive commission arrangements

- Inadequate disclosure of commission

- Certain types of tied lender arrangements

- Inadequate affordability checks

- Unfair selling practices

In addition to DCA complaints, regulators are continuing to look at undisclosed commissions and whether consumers were provided with sufficient information prior to entering agreements.

Consumers wanting broader guidance can also follow the latest car finance complaints updates as the FCA redress process develops.

DIY Complaints vs Solicitors vs Claims Management Companies

Consumers generally have three options when pursuing car finance compensation.

DIY Complaints

Some motorists choose to complain directly to lenders themselves.

This route is free and allows consumers to keep the full amount of any compensation awarded.

But it can be more challenging where:

- Agreements are old

- Documents are missing

- Deals were split between lenders

- Finance records are historic

- FCA eligibility rules apply

DIY complaints may be appropriate for consumers comfortable dealing with lenders themselves.

Solicitors and Law Firms

Some motorists prefer using solicitors, especially for more complex disputes.

Solicitors are regulated by the Solicitors Regulation Authority and may provide specialist legal expertise for difficult cases.

However:

- Fees may be higher

- Some firms only handle large or complex claims

- Not all law firms specialise in car finance claims

Claims Management Companies

Claims management companies are often chosen because they manage much of the process from start to finish.

The majority of regulated CMCs:

- Work on a no win no fee basis

- Trace agreements

- Deal with lender communication

- Submit complaints on your behalf

- Monitor updates from FCA redress

This means a less daunting and stressful process for the majority of motorists.

Consumers comparing providers can read more about regulated claims management companies before deciding which route feels right.

How Much Car Finance Compensation Could Be Available?

Compensation depends on:

- The agreement value

- The interest charged

- The commission structure involved

- Whether financial loss occurred

The FCA currently estimates:

- Average compensation for some older agreements may be around £734

- Average compensation for newer agreements may be around £881

- Overall average car finance refund estimates currently sit around £829

Some consumers may receive significantly more depending on the agreement and commission structure involved.

Which Lenders Are Most Commonly Linked to Complaints?

Complaints span a large part of the UK motor finance industry.

Some of the lenders most commonly linked to PCP car claims and car finance claims include:

Many Alphera customers say they were never given a clear explanation of how their interest rate was set. Some later discovered the rate seemed high for their credit profile and that commission had been factored in without their knowledge. Read more.

Drivers often assumed their dealership compared multiple lenders, only to learn later that Audi Finance was the default option. This sometimes resulted in rates that did not match the customer’s credit history or expectations. Read more.

Some customers report that fees and add-on costs were described vaguely or not broken down clearly. Others say commission was barely mentioned, which left them unsure how their final rate was determined. Read more.

Black Horse is one of the lenders most commonly mentioned when people talk about mis-selling. Many drivers say their interest rate was adjusted because of commission arrangements, yet nobody explained what this meant or how it affected the cost of the deal. A lot of customers recall feeling unsure about how their price was worked out, which is why transparency became such a concern in these complaints. Read more.

Blue Motor customers often mention rushed affordability checks or a lack of clarity around commission. Many say the conversation focused heavily on the monthly payment rather than the true cost of the agreement. Read more.

Complaints often centre on large balloon payments that were not fully explained. Some customers with strong credit histories also felt that their rates were higher than expected without a clear reason. Read more.

Drivers sometimes say they were not told how broker incentives worked or why certain fees appeared on the agreement. A lack of explanation at the point of sale is a common theme. Read more.

Close Brothers sat at the heart of the Supreme Court cases. Many customers say dealers increased their rate to earn more commission and that they were never told this could happen. Read more.

Clydesdale customers often mention vague fee descriptions and little to no disclosure about commission. Some only discovered years later that the dealer was financially incentivised to offer a certain product. Read more.

Honda customers frequently say balloon payments or mileage rules were brushed over rather than explained. Others say their interest rate felt higher than their credit score would suggest. Read more.

Many people say the interest rate they were given did not match their financial situation, and they were never shown how it was worked out. Others only learned later that commission may have shaped the deal, even though this was not explained at the time. Read more.

Many drivers report being offered rates that seemed unusually high without a clear explanation. Some say dealer incentives or commission were never discussed openly. Read more.

MotoNovo played a central role in the Supreme Court ruling. Customers often describe very limited disclosure around commission and quick explanations that did not allow them to understand how their deal was structured. Read more.

Northridge complaints often involve confusion about how rates were chosen. Some customers say fees were unclear or that the deal felt rushed on the day. Read more.

Some drivers discover add-ons in their paperwork that they do not remember talking through in any real detail. Others say the commission setup was touched on only briefly, leaving them without a clear sense of how it affected the price they paid. Read more.

Many say their APR was higher than they expected or that their rate changed during the process. Commission was rarely discussed in detail. Read more.

Many Toyota customers say the balloon payment or mileage rules were mentioned only in passing. These gaps in the explanation left some drivers facing costs they never expected when the agreement came to an end. Read more.

Some customers say the numbers they talked through in the showroom did not match what appeared later on the paperwork. Others only found out much later that commission had been added behind the scenes. Read more.

VW Finance customers often assumed the dealer shopped around the market. In reality, many deals were tied to a single lender. Complaints frequently involve inflated rates and undisclosed commission.Read more.

The FCA has not suggested that every agreement made with these lenders was unfair. However, firms across the industry either had discretionary commission arrangements in place before the ban in 2021 or work with dealerships through dealership networks where commission disclosure is now under increased scrutiny.

How the Industry Has Responded

Motor finance lenders have responded in different ways since the FCA redress scheme was announced.

Some firms expanded complaint handling teams and increased financial reserves in preparation for compensation payouts 2026. Others reviewed historic commission structures, dealership relationships, and internal sales practices linked to PCP and HP agreements.

Several organisations have also challenged parts of the FCA’s approach through legal action, including Consumer Voice [4] and a number of motor finance lenders questioning aspects of the redress framework.

Despite these disputes, the wider industry remains under intense scrutiny from regulators, consumer groups, the courts, and the media.

Frequently Asked Questions

What is the best PCP claims company?

The best PCP car finance claims company is usually one that specialises in motor finance complaints, explains fees clearly, operates transparently, and is authorised by the FCA.

What is the best car finance claims company?

The best car finance claims company should combine strong communication, specialist finance claims experts, clear no win no fee terms, and experience managing large volumes of complaints.

What's the difference between a solicitor and a claims management company?

Solicitors are regulated by the SRA and may be able to handle more legally complex disputes. Claims management companies are regulated by the FCA and often specialise in the handling of complaints and tracing of agreements.

Are claims management companies regulated?

Yes. Claims management companies dealing with regulated financial complaints are required to be authorised and supervised by the FCA.

Can I make a PCP claim without paperwork?

Yes. The majority of claims management companies have access to tracing agreements based on your name, date of birth and address history.

What is a car finance refund check?

A car finance refund check is an early eligibility review which aims to identify whether your agreement may have the potential to be eligible for compensation.

Are PCP claims legitimate?

Yes. In March 2026 the FCA formally launched a redress scheme after widespread mis-selling of car finance and unfair commission arrangements.

How long will car finance claims take?

Timescales vary depending on lender, complexity of agreement and FCA redress backlogs. Expect many claims to continue making progress in 2026 and 2027.

Is it too late to make a car finance claim?

No claims are too late to start, as agreements as far back as 2007 may still be eligible to a claim if the circumstances allow.

How do I avoid car finance claim scams?

Beware of any firm that guarantees a payout, does not mention fees, pressures consumers into signing up or will not explain FCA regulation when asked.

Final Thoughts

The FCA redress scheme has changed motorists’ attitudes to PCP claims and all car finance claims.

Millions of consumers are checking deals they signed between 2007 and 2024 to see if hidden commissions, high interest rates, or unfair sales techniques drove up the price of their finance.

Choosing the best car finance claim company can help simplify what is often a complex process, especially for consumers dealing with older agreements or missing paperwork.

If you believe your agreement may have been affected, starting a car finance refund check now may help you understand whether you could qualify for car finance compensation linked to mis-sold car finance.

Consumers wanting broader guidance on car finance mis-selling developments should continue monitoring FCA updates throughout 2026 and beyond.

_________

References:

- The Financial Conduct Authority formally launched its FCA redress scheme on 30 March 2026 - https://www.fca.org.uk/publications/policy-statements/ps26-3-motor-finance-consumer-redress-scheme

- Claims management companies dealing with regulated financial complaints must be authorised and regulated by the Financial Conduct Authority - https://www.fca.org.uk/firms/claims-management

- Law firms in England and Wales are regulated separately by the Solicitors Regulation Authority (SRA) - https://www.sra.org.uk/consumers/register/

- Several organisations have also challenged parts of the FCA’s approach through legal action, including Consumer Voice - https://consumervoice.uk/cars/fca-car-finance-compensation-challenge/